Student loans are an important way to finance tuition and other educational costs and can increase the probability of college persistence and graduation.[1] However, student loan debt can also be a challenge for students who do not complete a program of study and do not experience the boost in earnings that usually comes with a college degree. Paying off loans can be burdensome even for student borrowers who do graduate. As of 2025, there were about 42.8 million people holding $1.7 trillion in federal student loans, down from a peak of $1.9 trillion in 2020.[2]

Though community college students borrow less and generally have smaller balances than students in other sectors, they have their own struggles with debt. Community college students who do borrow default at somewhat higher rates than four-year college students and are less likely to resolve loan defaults. Student loan collection was paused during the COVID-19 pandemic but restarted in October 2023.

Since then, millions of student borrowers have fallen behind on their loans.[3] [4] In 2025, the federal government instituted new borrowing limits, changed the options for repayment, and cut back on loan forgiveness programs, but the new loan landscape is still taking shape.[5] [6]

What the Research Tells Us

Community college students are less likely to borrow than other college students and accrue less debt overall. The percentage of students who borrow has fallen in recent years but is still up over the longer term.

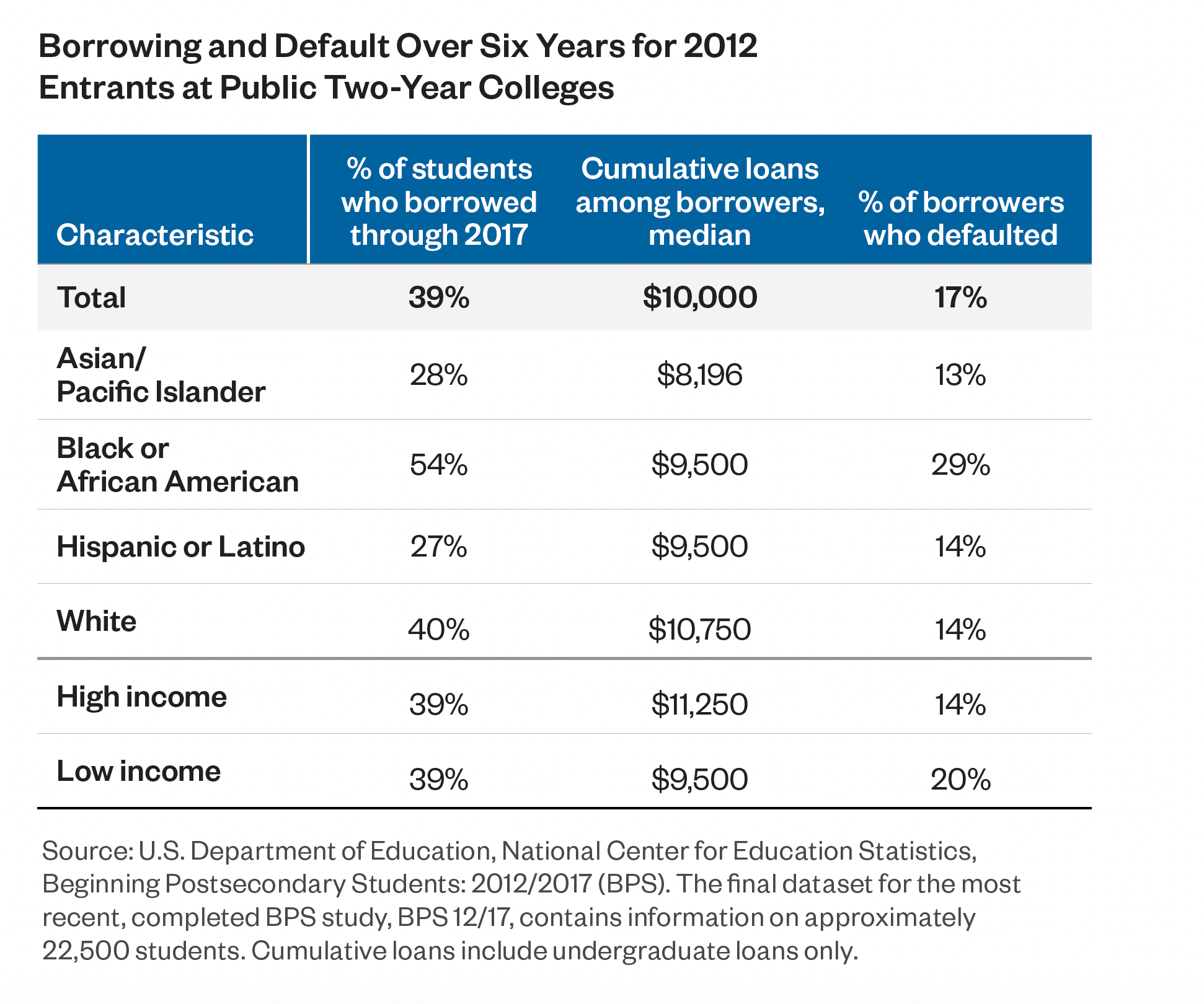

- Thirty-nine percent of public two-year college students who started in 2011-12[7] took out undergraduate loans within six years of college entry, and 17% of borrowers had defaulted on their loans within six years of college entry.[8]

- In 2019-20, 33% of associate degree graduates at public colleges had ever taken out loans, compared with 59% of bachelor’s graduates at public colleges. The average cumulative loan amount for associate graduates from public colleges who took out loans was $15,530.[9] [10]

- The share of community college students who took out student loans in a given year increased from 5% in 1999-2000 to 17% in 2011-12 and then decreased in 2019-20 to 11%. In 2019-20, the share of student borrowers at four-year public universities was 38% and at for-profit colleges was 62%.[11]

Many community college students appear to benefit from access to student loans, though they are often discouraged from borrowing.

- Colleges have discretion over whether to include loan offers in financial aid letters. Millions of community college students attend colleges that opt out of federal loan programs or do not include loan information in financial aid letters, even though most students would be eligible for loans.[12]

- Not surprisingly, access to loans increases borrowing at community colleges. Research indicates that students who borrow earn 3.7 more credits and their GPA increases by 0.6 points in their first year. Community college borrowers are also 11 percentage points more likely to transfer to four-year colleges one year later.[13]

- While access to loans may be better than not having access, grants may help even more. Students at colleges that offer federal loans appear to borrow less if they receive a Pell Grant. They also appear to reduce their work hours and take more credits.[14]

Community college borrowers default on their loans at higher rates than four-year college students. There are disparities in default by race and income.

- Student borrowers are more likely to default on their loans if they enroll part-time, never complete an associate or bachelor’s degree, or enroll only online.[15]

- Black students and low-income students have higher-than-average default rates.[16]

- Since the end of the pandemic student-loan payment pause, student borrowers are slower at paying down loan balances compared to before the pandemic, suggesting a looming increase in default rates.[17] [18] About 7.7 million federal student loan borrowers are in default, and more than 4 million borrowers are more than 30 days delinquent.[19]

- The cohort default rate (default within three years of entering repayment) for the 2017 cohort of community college student borrowers—the most recent unaffected by the payment pause—was 15.2%. Student borrowers at public four-year colleges defaulted at an average rate of 7.1%.[20] [21] [22]

- The most recent data on institutions at risk of losing access to federal student aid programs due to the percentage of borrowers who default on their loans shows that about two thirds are for-profit colleges and a quarter are public institutions.[23]

Policy Considerations

- Colleges should not discourage students from borrowing if it helps them complete their degrees in a timely fashion. The key is to help students borrow responsibly by calculating how much they can reasonably afford to pay back each month based on projected earnings and living expenses and to help students weigh their choice of program.

- Federal student loans generally offer better terms and greater protections than private loans or credit cards. Colleges should make clear that federal student loans are students’ best option.

- Still, loan defaults and delinquency might prevent students from returning to college and damage their finances. Policymakers should expand grant aid to ensure borrowing remains a supplement, not the foundation, of college financing.

- Colleges and the federal government should ensure that borrowers are aware of and can easily access income-contingent repayment after leaving college, to reduce the risk of default.

Endnotes

- Loans are in default when no payment has been made after 270 days.

- Hanson, M. (2026). Student loan debt statistics. Education Data Initiative. https://educationdata.org/student-loan-debt-statistics/

- U.S. Government Accountability Office. (2024, August 14). When the student loan payment pause ended, did borrowers pay? WatchBlog. https://www.gao.gov/blog/when-student-loan-payment-pause-ended-did-borrowers-pay

- Office of Federal Student Aid, U.S. Department of Education. (2026). Federal student aid posts updated reports to FSA data center. https://fsapartners.ed.gov/knowledge-center/library/electronic-announcements/2026-03-13/federal-student-aid-posts-updated-reports-fsa-data-center

- One Big Beautiful Bill Act. H.R.1, Public Law No. 119-21. (2025). https://www.congress.gov/bill/119th-congress/house-bill/1

- Moultrie, T. (2025, May 2). Hitting the brakes on a student loan default cliff. The Century Foundation. https://tcf.org/content/commentary/hitting-the-brakes-on-a-student-loan-default-cliff/

- Data for the 2011-12 cohort are the most recent available that include cumulative debt and repayment numbers.

- See table.

- National Center for Education Statistics (NCES). (2023). Percentage of undergraduate degree/certificate completers who ever received loans and average cumulative amount borrowed, by degree level, selected student characteristics, and institution control: Selected academic years, 1999-2000 through 2019-20 (Table 331.95). In Digest of Education Statistics. U.S. Department of Education, Institute of Education Sciences. https://nces.ed.gov/programs/digest/d23/tables/dt23_331.95.asp?current=yes

- Note that data from the National Postsecondary Student Aid Study does not follow a cohort over time; it captures cross-sectional snapshots.

- Looney, A., & Yannelis, C. (2024). What went wrong with federal student loans? Journal of Economic Perspectives, 38 (3), 209–36. https://www.aeaweb.org/articles?id=10.1257/jep.38.3.209

- Marx, B. M., & Turner, L. J. (2019). Student loan nudges: Experimental evidence on borrowing and educational attainment. American Economic Journal: Economic Policy 11(2), 108–141. https://www.aeaweb.org/articles?id=10.1257/pol.20180279

- Marx & Turner (2019).

- Park, R. S. E., & Scott-Clayton, J. (2018). The impact of Pell Grant eligibility on community college students’ financial aid packages, labor supply, and academic outcomes. Educational Evaluation and Policy Analysis, 40(4), 557–585. https://doi.org/10.3102/0162373718783868

- Levine, I., Takyi-Laryea, A., Oliff, P., & West, L. (2024, January 30). Borrowers with certain educational experiences appear more likely to default. The Pew Charitable Trusts. https://www.pew.org/en/research-and-analysis/articles/2024/01/30/borrowers-with-certain-educational-experiences-appear-more-likely-to-default

- See table.

- U.S. Government Accountability Office. (2024). Federal student loans: Preliminary observations on borrower repayment practices after the payment pause. https://www.gao.gov/assets/gao-24-107150.pdf

- Cohn, J. (2026). Student loan repayment since the payment restart: Using credit bureau data to assess borrower progress. Urban Institute. http://urban.org/sites/default/files/2026-01/Final_Student_Loan_Repyament_Since_the_Payment_Restart.pdf

- Office of Federal Student Aid (2026).

- NCES. (2022). Number of postsecondary students who entered the student loan repayment phase, number of students who defaulted within a 3-year period, and 3-year student loan cohort default rate, by level and control of institution: Fiscal years 2010 through 2019 (Table 332.50). In Digest of Education Statistics. U.S. Department of Education, Institute of Education Sciences. https://nces.ed.gov/programs/digest/d22/tables/dt22_332.50.asp

- Association of Community College Trustees. (n.d.). Student loan cohort default rates and community colleges – FAQs. https://acct.org/sites/default/files/documents/2025-05/ACCT%20FAQ%20Student%20Loan%20Default%205.14.25%20Final.pdf

- Office of Federal Student Aid, U.S. Department of Education. (2020, September 30). FY 2017 Official national cohort default rates with prior year comparison and total dollars as of the date of default and repayment [Briefing]. https://fsapartners.ed.gov/knowledge-center/library/electronic-announcements/2020-09-30/national-default-rate-briefing-fy-2017-official-cohort-default-rates

- Alonso, J. (2026, February 24). ED warns colleges with high student loan nonrepayment rates. Inside Higher Ed. https://www.insidehighered.com/news/students/financial-aid/2026/02/24/ed-warns-colleges-high-student-loan-nonrepayment-rates